Q3 2021 Financial Update

Quarterly Market Commentary: Third Quarter 2021

Markets Struggle in the Third Quarter

Global equity markets had a mixed third quarter, but when the final Wall Street-bell chimed on September 30th, global markets had not moved very much, despite the final month of the quarter turning in dismal results.

For the third quarter of 2021:

The DJIA ended 3Q with a loss of 1.5%;

The S&P 500 ended 3Q with a gain of 0.6%;

NASDAQ ended 3Q with a loss of 0.2%; and

The Russell 2000 ended 3Q with a loss of 4.4%.

But many are trying not to focus on the mixed returns for 3Q (and dismal September returns) and are instead focusing on how the market performed for the first nine months of the year – and those numbers are solid, as:

The DJIA is up 12.1% YTD;

The S&P 500 is up 15.9% YTD;

NASDAQ is up 12.7% YTD; and

The Russell 2000 is up 12.4% YTD.

Interestingly, the themes that helped drive market performance have been on Wall Street’s worry list for a while and did not just appear on July 1st. Topping the worry list was rising inflation, the Federal Reserve’s schedule of remaining accommodative; declining consumer sentiment; overheating housing; concerns that the delta variant might stall economic activity; and disappointing economic data hampered by supply chain issues.

Further, we saw that:

Volatility, as measured by the VIX, trended up in the third quarter, starting slightly over 15 and ending the month at 23.

West Texas Intermediate crude did not move much in the third quarter, starting and ending just north of $75/barrel. Further, WTI has climbed more than 50% in six months, having started 2021 at $48/barrel.

Market Performance Around the World

Investors were not thrilled with the quarterly performance around the world, as 32 of the 35 developed markets tracked by MSCI were negative for the third quarter of the year. And of the 40 developing markets tracked by MSCI, 26 of them were negative too.

Source: MSCI. Past performance cannot guarantee future results

Again, the themes that helped drive market performance this month have been on Wall Street’s worry list for a long time and did not magically appear when the third quarter kicked off.

In fact, the worries of rising inflation; the Federal Reserve’s schedule of remaining accommodative; declining consumer sentiment; overheating housing; the delta variant; and supply chain issues have all been around for many months (inflation has gone up every month in 2021, for example).

But the third quarter did see a few more troublesome topics added to that long worry list, including:

Treasury Secretary Janet Yellen warning of economic catastrophe if Congress did not raise the debt ceiling limit;

A hotly-debated infrastructure bill that could carry a price tag of at least $1 trillion and up to $3.5 trillion;

Skyrocketing shipping fees heading into the holiday season as container ships are anchored outside U.S. ports waiting to be unloaded;

Rising unemployment applications for the last 3 weeks of the month; and

China’s Evergrande Group risking default on its debt and sending shock-waves throughout global markets, similar to when Lehman Brothers collapsed (13 years ago to the day) and kicked off the Financial Crisis of 2008.

And as if we need another reminder about inflation, the number of companies warning of inflation on their latest earnings calls hit an all-time high too.

Finally, while glass-half-empty economists were busy reminding us all month that September has historically the worst month for stocks, now they’re preaching that October has historically been the most volatile month for stocks. So, is it any surprise that stocks struggled with this growing Wall of Worry?

September Lived Up to Its Billing

All the major U.S. equity markets and virtually all the developed and emerging markets tracked by MSCI were down for the month of September, in keeping in line with what has historically been the worst month for stocks. For the month of September:

The DJIA was down 4.3%;

The S&P 500 was down 4.8%;

NASDAQ was down 5.3%; and

The Russell 2000 was down 3.6%.

Further, the S&P 500 and NASDAQ both turned in their worst months since the height of the pandemic in March 2020.

IPOs on Fire

The IPO market was on fire during the third quarter, with a stunning record amount of activity on the M&A and IPO front. Here are some statistics for perspective:

Q3’s global M&A activity produced deals worth more than $1.5 trillion, which is 38% more than the highest quarter on record

Global M&A activity through the first nine months of 2021 reached more than $4.3 trillion, which trounces the annual record of $4.1 trillion

There has been a crazily historic 770 U.S. IPOs over the first three quarters of 2021 and that is a whopping 3x the ten-year average of 205

SPACs make up 58% of this year’s IPOs, but the 323 non-SPAC IPOs are already greater than any year since 2008

Sector Performance Rotated in Q32021

The overall trend for sector performance for each of the first nine months and the first, second and third quarters was good, but the performance leaders and laggards did rotate throughout, suggesting that a few sector rotations may have occurred in just 9 months.

For perspective, recall that this time last year, the third quarter of 2020 ended with 10 of the 11 S&P 500 sectors painted green. Fast forward a year later and 5 of the 11 are painted red.

Here are the sector returns for the shorter time periods:

Source: FMR

Reviewing the sector returns for just the third quarter of 2021, we saw that:

5 of the 11 sectors were painted green for the third quarter;

The Energy sector turned in another volatile quarter, this time retreating as the price of oil barely moved, whereas last quarter Energy led the other sectors as the price of oil leapt by $15/barrel;

The Financials sector turned in another solid quarter, helped by the Federal Reserve’s stance of keeping rates low through at least 2023; and

The differences between the best (+2.77%) performing and worst (-3.71%) performing sectors in the third quarter widened.

Asset Class & Style Performance

The second quarter and first six months of 2021 were good for almost all investors, with most of the major asset classes and styles turning in very respectable – and most importantly green – numbers across the board.

For the quarter, Commodities continued their spectacularly red-hot pace, Growth outpaced Value and small-caps lagged the larger caps.

Source: Barclays, Bloomberg, FactSet, FTSE, MSCI, J.P. Morgan Asset Management. DM Equities: MSCI World; REITs: FTSE NAREIT All REITs; Cmdty: Bloomberg UBS Commodity Index; Global Agg: Barclays Global Aggregate; Growth: MSCI World Growth; Value: MSCI World Value; Small cap: MSCI World Small Cap. All indices are total return in local currency. Past performance is not a reliable indicator of current and future results.

Turning to Commodities, which jumped another 6% for the quarter to add to its almost 30% gain YTD, it should be noted that 14 of the last 17 months have seen gains. Further, that almost 30% gain YTD represents its largest annual gain since 1979.

Natural gas has gone through the roof with a YTD gain of 135% and WTI Crude oil is up 55% YTD. Supply and demand challenges are driving energy prices higher, as the summer driving season saw record-high gasoline demand and supplies were disrupted by hurricane season.

Consumer Confidence Sinks Again

On September 28th, the Conference Board announced that its Consumer Confidence Index declined in September, after declining in both July and August. The Index now stands at 109.3 (1985=100), down from 115.2 in August. And only 19% of consumers think business conditions are good, whereas 25% think conditions are bad.

“Concerns about the state of the economy and short-term growth prospects deepened, while spending intentions for homes, autos, and major appliances all retreated again. Short-term inflation concerns eased somewhat, but remain elevated,” read the press release from the Conference Board.

Inflation Keeps Rising

The Bureau of Labor Statistics reported that the Consumer Price Index for All Urban Consumers increased 0.3% in August on a seasonally adjusted basis after rising 0.5% in July. Over the last 12 months, the All Items index increased 5.3%.

A few highlights:

The indexes for gasoline, household furnishings and operations, food, and shelter all rose in August and contributed to the monthly all items seasonally adjusted increase.

The energy index increased 2.0%, mainly due to a 2.8% increase in the gasoline index.

The index for food rose 0.4%, with the indexes for food at home and food away from home both increasing 0.4%.

Some Positive Inflation News Maybe?

Here is some good news on the monthly inflation increases (maybe):

The index for dairy and related products declined in August, falling 1.0% after rising in each of the previous 4 months.

There was a sharp decline in the index for food at employee sites and schools, which fell 17% in August.

The index for airline fares fell sharply, decreasing 9.1% over the month.

The index for used cars and trucks declined 1.5% in August, ending a series of five consecutive monthly increases.

GDP Up 6.7%

On the last day of the third quarter, the Bureau of Economic Analysis announced that real gross domestic product increased at an annual rate of 6.7% in the second quarter. In the first quarter, real GDP increased 6.3 percent.

“The increase in real GDP in the second quarter reflected increases in PCE, nonresidential fixed investment, exports, and state and local government spending that were partly offset by decreases in private inventory investment, residential fixed investment, and federal government spending. Imports, which are a subtraction in the calculation of GDP, increased.”

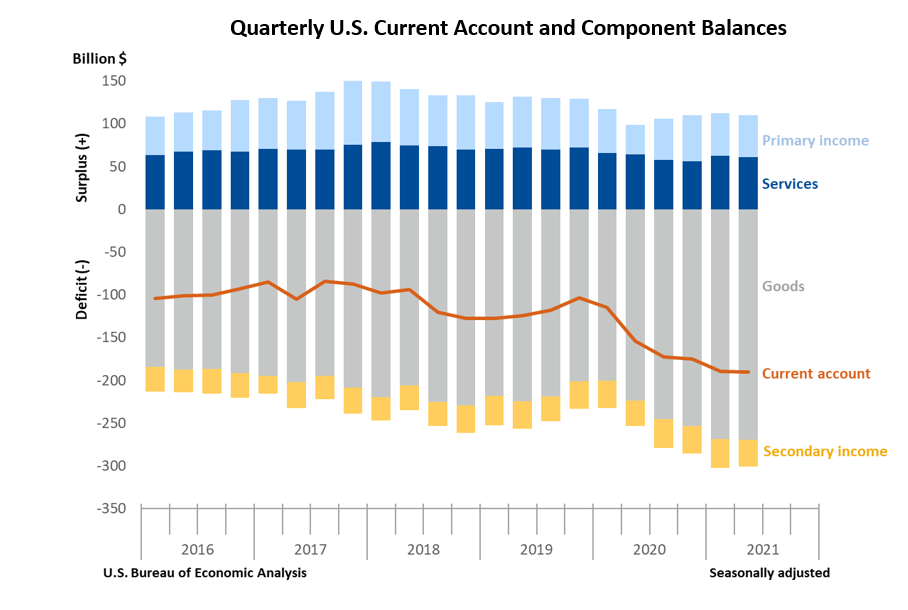

Current Account Deficit Widens in 2Q

The U.S. Bureau of Economic Analysis announced that “the U.S. current account deficit, which reflects the combined balances on trade in goods and services and income flows between U.S. residents and residents of other countries, widened by $0.9 billion, or 0.5%, to $190.3 billion in the second quarter of 2021.

The second quarter deficit was 3.3% of current dollar gross domestic product, down from 3.4% in the first quarter. The $0.9 billion widening of the current account deficit in the second quarter mainly reflected reduced surpluses on services and on primary income that were mostly offset by a reduced deficit on secondary income.”

Jobless Claims Up

On the last day of the quarter, the Department of Labor announced that for the week ending September 25th, the advance figure for seasonally adjusted initial claims was 362,000, an increase of 11,000 from the previous week's unrevised level of 351,000. In addition:

the 4-week moving average was 340,000, an increase of 4,250 from the previous week's unrevised average of 335,750.

The advance seasonally adjusted insured unemployment rate was 2.0% for the week ending September 18, a decrease of 0.1% from the previous week's unrevised rate.

The advance number for seasonally adjusted insured unemployment during the week ending September 18 was 2,802,000, a decrease of 18,000 from the previous week's revised level.

The 4-week moving average was 2,797,250, a decrease of 750 from the previous week's revised average. This is the lowest level for this average since March 21, 2020 when it was 2,071,750.

“The highest insured unemployment rates in the week ending September 11 were in Puerto Rico (4.7), California (3.4), District of Columbia (3.2), Oregon (3.2), Alaska (3.1), Nevada (3.1), New Jersey (3.1), the Virgin Islands (3.1), Hawaii (2.7), and Illinois (2.7).

The largest increases in initial claims for the week ending September 18 were in California (+17,218), Virginia (+12,140), Ohio (+4,147), Oregon (+3,413), and Maryland (+2,452), while the largest decreases were in Louisiana (-6,935), New York (-2,275), Missouri (-1,568), Oklahoma (-1,264), and New Mexico (-1,055).”

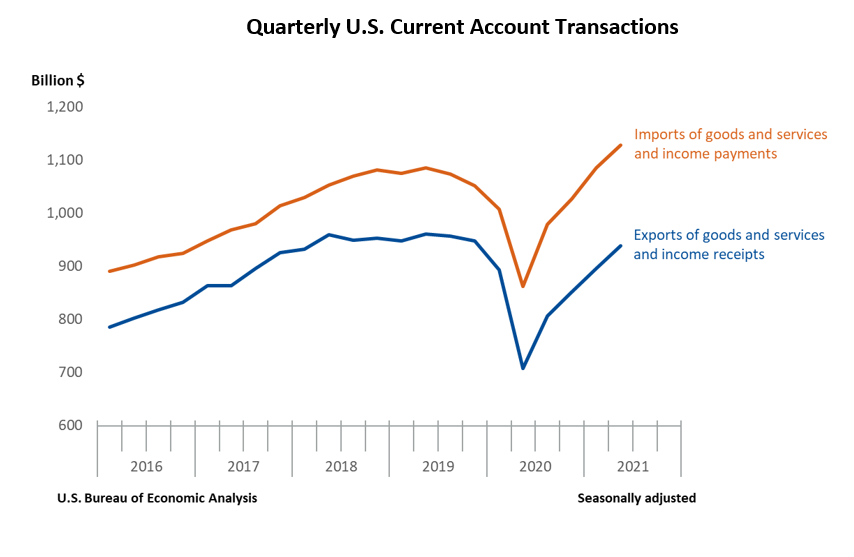

Exports & Imports of Goods and Services

“Exports of goods increased $28.3 billion, to $436.6 billion, mostly reflecting increases in industrial supplies and materials, mainly petroleum and products, and in capital goods, mainly civilian aircraft and semiconductors.

Imports of goods increased $29.0 billion, to $706.3 billion, primarily reflecting an increase in industrial supplies and materials, mainly petroleum and products and metals and nonmetallic products.

Exports of services increased $7.6 billion, to $189.1 billion, primarily reflecting an increase in travel, mostly other personal travel.

Imports of services increased $9.1 billion, to $127.8 billion, mostly reflecting increases in transport, primarily sea freight and air passenger transport, and in travel, primarily other personal travel.”

Worries of a Government Shutdown?

On literally the last day of the month with just hours to spare, President Biden signed a bill extending government funding through December 3rd, averting a partial shutdown. But the debt-ceiling fight remains and is likely to dominate Wall Street’s Wall of Worry heading into October.

Here is a very important thing to remember: if the debt ceiling is not raised and the government does shut down, it wouldn’t be the first time. In fact, it wouldn’t even be the twentieth time.

Since 1976 the government has been shut down 22 times, the last being between December 22, 2018 until January 25, 2019 (35 days). If this happens, then yes, the stock market will likely react negatively.

But for perspective, consider the impact to stock markets during the last 2013 and 2018/2019 shutdowns – stocks actually rose.

Source: FactSet

But remember, as always: past performance is never a guarantee of future results.

Sources: census.gov; bea.gov; bls.gov; dol.gov; bea.gov; factset.com; msci.com; fidelity.com; nasdaq.com; wsj.com; morningstar.com